Half to 13. 125 percent.3 GILTI, nevertheless, is not restricted to low-taxed revenue and also incorporates income based on international tax rates over of 13. 125 percent. Because of this, double taxes can arise because of the GILTI foreign tax credit (FTC) limitations4 and the lack of a legal high-tax exemption equivalent to that consisted of in the Subpart F arrangements (under Section 954(b)( 4 )).

Department of the Treasury as well as IRS to give a regulative high-tax exemption.5 The Treasury Division and also IRS released recommended laws in 2019, which provided a GILTI high-tax exemption, as follows: The high-tax exception was elective by a CFC’s controlling domestic shareholders, binding on all U.S. investors of the CFC, as well as as soon as made or revoked, could not be changed for a 60-month period.

9 percent (i. e., in extra of 90 percent of the highest possible UNITED STATE corporate tax price, which is 21 percent). Foreign tax prices were determined individually with respect to each certified service device (QBU) of a CFC to seize mixing of high-taxed and low-taxed revenue, and might not be applied on a CFC-by-CFC basis.

Last Rules The IRS issued the GILTI high-tax exclusion last guidelines on July 20, 2020, which were published on July 23, 2020, in the Federal Register. Amongst the bottom lines are: Political election: Now on an basis; 60-month rule dropped. Election made on income tax return or on changed return by affixing a declaration.

Managing The Us Tax Impact Of Highly-taxed Foreign Subsidiaries in Honolulu, Hawaii

Decision: Now based on “Tested Unit” rather than QBU-by-QBU basis. Based on publications and records, and gross earnings determined under federal earnings tax principles with specific adjustments to mirror neglected settlements, which serves as a sensible proxy for figuring out the amount of gross earnings that the foreign country of the evaluated device is likely topic to tax.

All examined devices of a CFC situated or resident in very same country are required to be incorporated as a single checked unit. Typically puts on extent an entity undergoes tax in foreign country as well as in the Treasury Department and also Internal Revenue Service view is much more targeted than QBU approach. Decisions will be complicated.

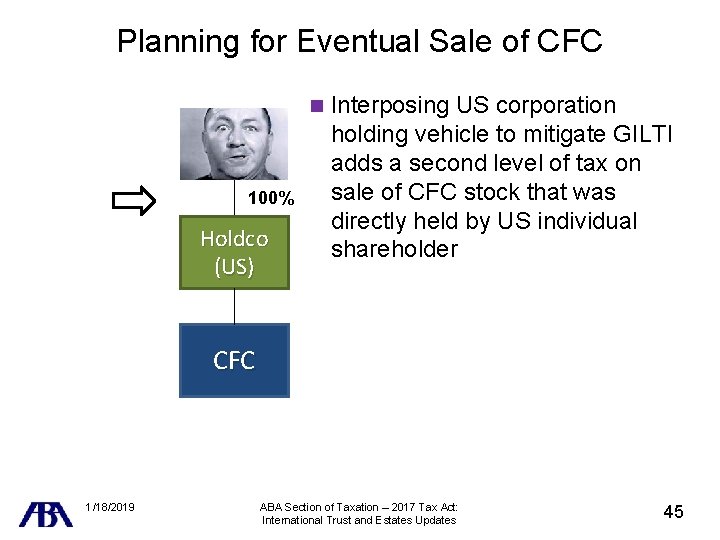

Private shareholders need to examine whether a high-tax kick-out political election is much more advantageous compared to intending under Section 962, use a domestic company (if readily available and also can prevent residential penalty tax guidelines) or check-the-box planning where the investors elects to deal with the CFC as transparent as well as revenue and FTCs of the CFC pass through to the shareholders.

corporate revenue tax, assuming no appropriation or apportionment of costs. 4 80 percent usage of FTCs, different restriction basket and also no carryback or continue. 5 To be consistent with the law, the final GILTI regulations provided on June 21, 2019, offered that the exclusion of high-taxed earnings from checked income under the GILTI rules uses just with respect to earnings that otherwise would have been tired as Subpart F income entirely but also for the application of the high-tax exception to Subpart F earnings under Section 954(b)( 4 ).

Taking The Sting Out Of Mandatory Repatriation – Global Tax … in Portsmouth, New Hampshire

Going ahead, the Subpart F high-tax exception will apply on a checked system basis and also can only be made on a “unitary” basis; i. e., both for Subpart F as well as GILTI objectives. Info had in this alert is for the basic education and learning as well as understanding of our readers. It is not made to be, as well as need to not be made use of as, the single resource of information when examining as well as settling a legal trouble.

Classifying Your Business It is very important to maintain in mind hereof that the classification of companies under the tax law of your country might not concur with the category for UNITED STATE tax objectives. For example, entities that are ruled out companies under international law may be considered corporations for U.S.

In addition, other code arrangements are relevant under the CFC program, consisting of, connecting to financial investments in U.S. residential property (which include, importantly, loans to UNITED STATE investors) by CFCs that can cause an existing addition in an U.S. Investor’s gross earnings. A CFC is technically specified as any international (i. e., non-U.S.) company, if greater than 50% of (i) the complete combined voting power of all classes of supply of such company qualified to vote; or (ii) the total worth of the shares in such firm, is had in the accumulation, or is considered as owned by applying certain attribution policies, by United States Shareholders on any kind of day throughout the taxed year of such international firm.

Should You Set Up A Foreign Entity For Your Ico? – Crowell … in Little Rock, Arkansas

person that possesses, or is thought about as owning, by using certain acknowledgment guidelines, 10 percent or more of the total ballot power or the overall value of shares in the foreign company. CFCs and also the Subpart F Regulations As gone over over, the Subpart F rules attempt to avoid deflection of income from the United States right into another territory, especially one which has a special tax program.

g., rewards, rate of interest, aristocracies) earnings, the GILTI regulations are aimed at a CFC’s active (e. g., service, trading) revenue. In basic, GILTI is computed as the revenue of the CFC (aggregated for all the CFCs had by the U.S. investor) that remains in extra of a 10% return on specific substantial residential property of the CFC.

125%. An U.S. person, on the various other hand, will certainly be strained at the ordinary tax price on such GILTI (37% is the maximum price) with no 50% reduction and also no foreign tax credit for the international tax paid at the CFC level. For this reason, a private U.S. shareholder who holds at the very least 10% of the CFC should think about making a so-called “962 election” to be taxed as a company on the GILTI (i.

Founded in 2015 and located on Avenue of the Americas, in the heart of New York City, International Wealth Tax Advisors provides highly personalized, secure and private global tax, GILTI, FATCA, Foreign Trusts consulting and accounting to many clients worldwide, including: Singapore, IWTAS.com China, Mexico, Ecuador, Peru, Brazil, Argentina, Saudi Arabia, Pakistan, Afghanistan, South Africa, United Kingdom, France, Spain, Switzerland, Australia and New Zealand.

Such an election can have complicated and also differed tax repercussions, and a tax advisor must be consulted to fully comprehend its values. Presently, the IRS and also Treasury Department are considering executing a so-called “high-tax exemption”, which would excuse a CFC from the GILTI guidelines if the company is tired in your area at a price more than 18.

Cfc Tax Planning For U.s. Individuals And Family Offices – Step in Grapevine, Texas

Rules carrying out the high-tax exemption are currently in proposed kind as well as have not yet been settled. CFCs as well as the Reporting Policy People who own CFCs need to include Form 5471 with their federal tax return. There are also a number of various other comparable categories of filers that must submit this type. Special acknowledgment rules (that include attribution in between partners) might relate to expand the extent of taxpayers that drop within these groups.

If the info is not submitted within 90 days after the Internal Revenue Service has mailed a notice of the failing to the UNITED STATE individual, an extra $10,000 charge (per international corporation) is charged for every 30-day period, or portion thereof, throughout which the failure continues after the 90-day period has run out.

This can be the situation even if such funds are held with a tax-deferred cost savings account (e. g., U.K.

In Review: Corporate Tax Planning Developments In Usa in Alhambra, California

Under the mark-to-market election, shareholders must investors need to year as ordinary incomeAverage earnings excess of the fair market reasonable of the PFIC stock as supply the close of the tax year over its adjusted basis in the shareholders booksInvestors If the stock has declined in value, a common loss deduction is allowed, but it is restricted to the quantity of gain previously consisted of in earnings.

Carrying out PFIC calculations for firms and also investors that have not been accumulating the called for details from the beginning can be very difficult, if not difficult, depending upon the details offered. Unlike various other information returns, Type 8621 does not bring a penalty for not submitting the type. Nevertheless, failing to file the form does leave open the statute of constraints on all tax matters for that tax year forever.

Area 965 does not distinguish U.S. business investors from various other U.S. international tax attorney. investors, so the shift tax potentially uses to any UNITED STATE

Worldwide Corporate Tax Guide – Ey in Boise, Idaho

Other aspects of Area 965 that could possibly reduce the discomfort of the transition tax including the following: UNITED STATE shareholders can choose to pay the shift tax over a duration of up to 8 years.

investor are reduced (yet not listed below absolutely no) by the investor’s share of shortages from various other specified international companies. The shift tax does not put on previously-taxed incomes and also revenues. The section of revenues based on the shift tax does not include E&P that were collected by an international business before attaining its standing as a specified foreign corporation.

investors (as specified in Area 951(b)), the characterization of the distribution for UNITED STATE tax functions will depend in part on whether the CFC has any revenues as well as revenues (E&P), as well as, if it does, the kind of E&P being dispersed. Assuming the CFC has E&P, such distribution will certainly first be a distribution of previously exhausted revenues and also earnings (PTEP) followed by a distribution of non-PTEP.

To the extent that the withholding taxes are enforced (or various other international tax obligations have formerly been imposed) on a distribution of PTEP, a taxpayer will need to determine whether (as well as to what degree) such foreign taxes may be worthy. A number of unique policies might use. An U.S. shareholder additionally might be entitled to a rise in its Section 904 foreign tax credit limitation under Area 960(c).

The Gilti High-tax Exception: Is It A Viable Planning Option? in Bethesda, Maryland

Taxpayers must keep in mind that under Section 245A(d), no debt or reduction is enabled for any kind of foreign tax obligations paid or accumulated (or treated as paid or accrued) with respect to any type of returns for which the Area 245A DRD is allowed. Individual investors will certainly wish to validate whether they can declare professional returns tax prices under Section 1(h)( 11) on such returns.

shareholders ought to validate the quantity of basis in their CFC supply (if various blocks of supply exist, the basis in each block of supply) to figure out the amount of the distribution that can be gotten tax-free under Area 301(c)( 2 ). If a CFC distribution exceeds the CFC’s E&P as well as the U.S.

Like actual circulations, taxpayers will certainly need to analyze as well as compute the relevant E&P in the CFC to determine the tax implications of the CFC loans. To the extent the CFC has PTEP that is not being dispersed, such PTEP may be able to protect the UNITED STATE investor from an income inclusion under Section 951(a).

Unless an exemption applies (e. g., the de minimis exception under Area 954(b)( 3 ), the high taxed exemption under Area 954(b)( 4 ), etc.), passion received by the CFC needs to typically be Subpart F income and includible right into gross revenue by the U.S

Passion paid to the CFC needs to typically be subject to a 30% UNITED STATE keeping tax unless reduced by an earnings tax treaty.

International Wealth Tax Advisors, LLC

1270 6th Ave 7th floor,New York, NY 10020, USA

g., foreign ignored entities) will certainly need to think about the tax implications of such circulations. Are there any kind of international withholding tax obligations on such distributions? To the level that the distribution is from a “professional business unit” that is on a various practical money than the U.S. taxpayer, foreign money exchange gain or loss may be acknowledged under Area 987.